Embark on a journey towards financial freedom with our step-by-step guide, “The Road to Zero Debit.” Discover the path to eliminating debt and achieving a more secure financial future.

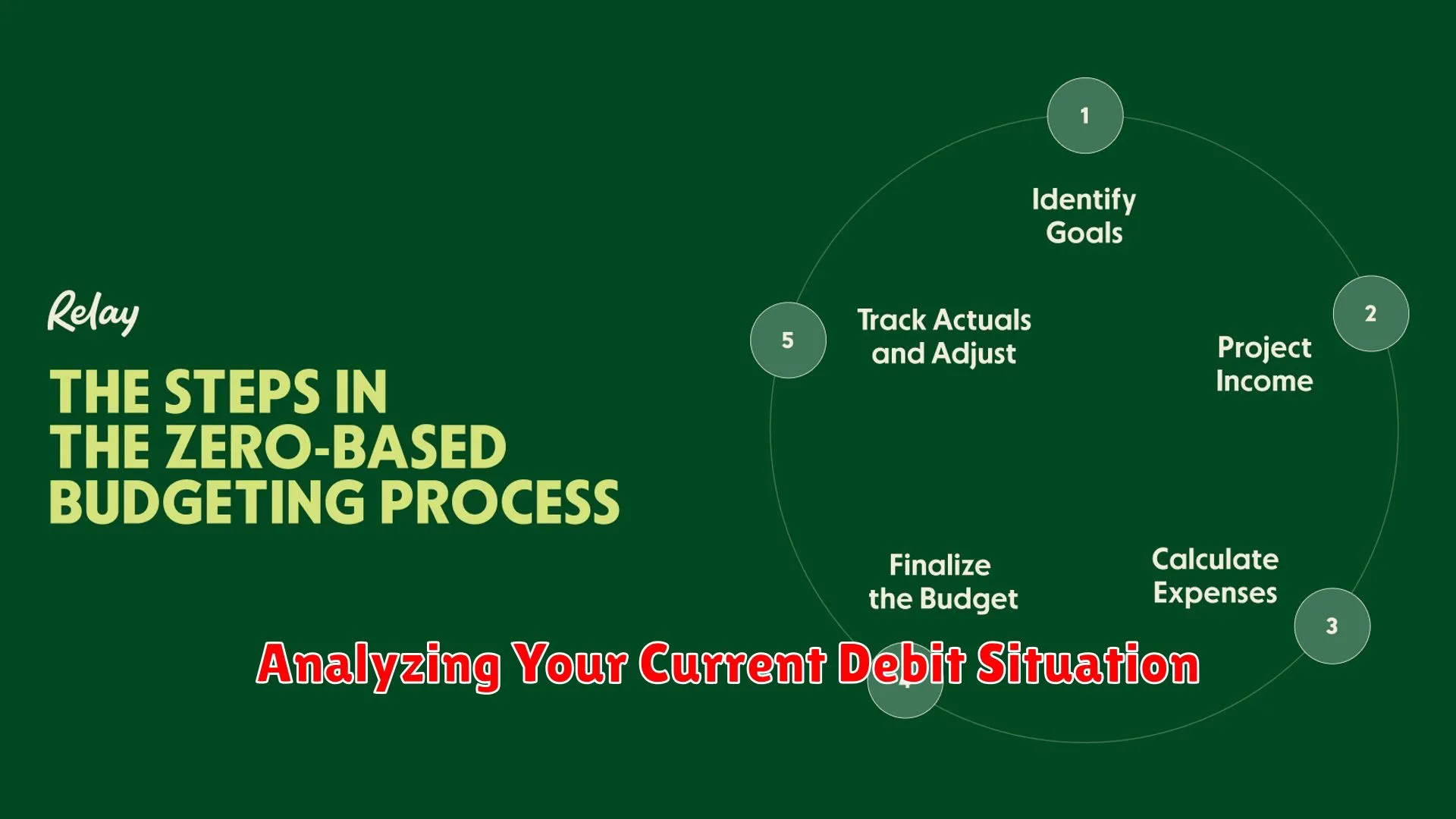

Analyzing Your Current Debit Situation

Understanding your current debit situation is the crucial first step on the road to zero debit. Start by examining your bank statements and tracking your spending habits.

Look closely at your income and expenses to determine where your money is going each month. Highlight any unnecessary or impulse purchases that contribute to your current debit level.

Consider categorizing your expenses into essential (such as groceries, rent, and bills) and non-essential (like dining out, shopping for luxury items). This categorization can help you identify areas where you can cut back.

Review your current debt balances, including credit cards and outstanding loans. Make a list of all your debts, including the interest rates and minimum payments. Understanding the full scope of your debt will help you create a plan to tackle it.

Assess your spending patterns and identify any triggers that lead to impulse purchases or unnecessary expenses. This self-awareness is key to making positive changes towards financial stability.

Strategies for Tackling High-Interest Debit First

When embarking on the journey towards zero debit, one of the crucial steps is to prioritize tackling high-interest debt first. This strategic approach can help you save money on interest payments and accelerate your path towards financial freedom. Here are some effective strategies to help you tackle high-interest debit:

1. Create a Debt Repayment Plan

Start by listing all your debts, highlighting the ones with the highest interest rates. Develop a repayment plan that allocates extra funds towards paying off these high-interest debts while making minimum payments on others. This targeted approach will help you eliminate costly debt sooner.

2. Consider Balance Transfers or Debt Consolidation

If feasible, explore options like balance transfers to lower interest rate cards or consolidating high-interest debts into a single, more manageable loan. Be mindful of any associated fees and ensure that the new terms are advantageous in the long run.

3. Increase Your Income and Cut Expenses

Boost your income through side hustles, freelance work, or selling unused items to allocate more funds towards debt repayment. Simultaneously, review your budget and identify areas where you can cut back expenses to free up additional funds for paying off high-interest debts.

4. Prioritize Discipline and Persistence

Staying committed to your debt repayment plan and resisting the temptation to accumulate more debt are key to successfully tackling high-interest debt. Celebrate small victories along the way to stay motivated and maintain discipline in your financial journey.

How to Utilize the Snowball Method

The Snowball Method is a popular strategy to pay off debt efficiently and stay motivated along the way. Here’s a step-by-step guide on how to effectively utilize this method:

- List Your Debts: Start by listing all your debts from smallest to largest, regardless of interest rates. This will help you have a clear overview of what needs to be paid off.

- Minimum Payments: Make minimum payments on all your debts except the smallest one. Put any extra funds towards paying off the smallest debt first.

- Snowball Effect: Once the smallest debt is paid off, take the money you were putting towards it and add it to the minimum payment of the next smallest debt. This creates a snowball effect, accelerating your debt repayment.

- Repeat and Refocus: Keep repeating this process as each debt is paid off. Stay focused and committed to the plan, celebrating each milestone along the way.

- Stay Motivated: Seeing your debts decrease one by one can be incredibly motivating. Use this momentum to stay on track and keep working towards becoming debt-free.

The Impact of Debit on Credit Scores

When it comes to managing your finances and striving for a healthy financial future, understanding the impact of debit on your credit scores is crucial. While debit cards are convenient for daily transactions and can help you avoid debt, they don’t directly impact your credit score. This is because debit card transactions are not reported to the major credit bureaus.

However, there are indirect ways in which using a debit card can affect your credit scores. One key aspect is responsible spending habits. By using your debit card wisely and keeping your bank account in good standing, you demonstrate financial responsibility, which can have a positive impact on your creditworthiness in the long run.

Additionally, if you link your debit card to a savings account or use it in conjunction with budgeting tools, you can better track your spending and avoid overspending, which can indirectly benefit your credit scores by preventing financial distress and missed payments.

While debit cards may not directly boost your credit scores, managing your finances well through responsible debit card usage can contribute to your overall financial health and potentially pave the way for a stronger credit profile in the future.

Maintaining a Zero Debit Lifestyle

Living a zero debit lifestyle is a financial goal that can provide a sense of security and freedom from debt. It involves managing your finances in a way that ensures you don’t accumulate any debt, and if you do have debt, paying it off quickly. Here are some key steps to help you maintain a zero debit lifestyle:

- Create a Budget: Start by creating a detailed budget that outlines your income and expenses. Make sure to include all monthly bills, groceries, savings, and any other spending categories. This will give you a clear picture of where your money is going and help you identify areas where you can cut back.

- Track Your Spending: Keep track of every dollar you spend to ensure that you are staying within your budget. This can be done through apps, spreadsheets, or even just pen and paper. By monitoring your spending habits, you can make adjustments as needed to prevent overspending.

- Build an Emergency Fund: Having an emergency fund can prevent you from going into debt in case of unexpected expenses, such as car repairs or medical bills. Aim to save at least three to six months’ worth of living expenses in your emergency fund.

- Avoid Impulse Purchases: Before making a purchase, especially a large one, take some time to think it over. Consider if it’s a necessity or a want. If it’s the latter, give yourself a grace period before making the purchase to avoid impulse buying.

- Pay Off Debt Strategically: If you have existing debt, focus on paying it off strategically. Consider using the debt snowball or debt avalanche method to tackle your debts efficiently. Make extra payments whenever possible to accelerate the payoff process.

By following these steps and staying disciplined with your financial habits, you can work towards maintaining a zero debit lifestyle and enjoy the peace of mind that comes with being debt-free.

Conclusion

Following this step-by-step guide will lead you towards achieving zero debit and financial freedom.

{kind=link}