In this article, we will explore effective strategies to break free from the debit cycle and pave the way towards a more promising financial future. Learn how to manage your finances wisely and take control of your economic well-being.

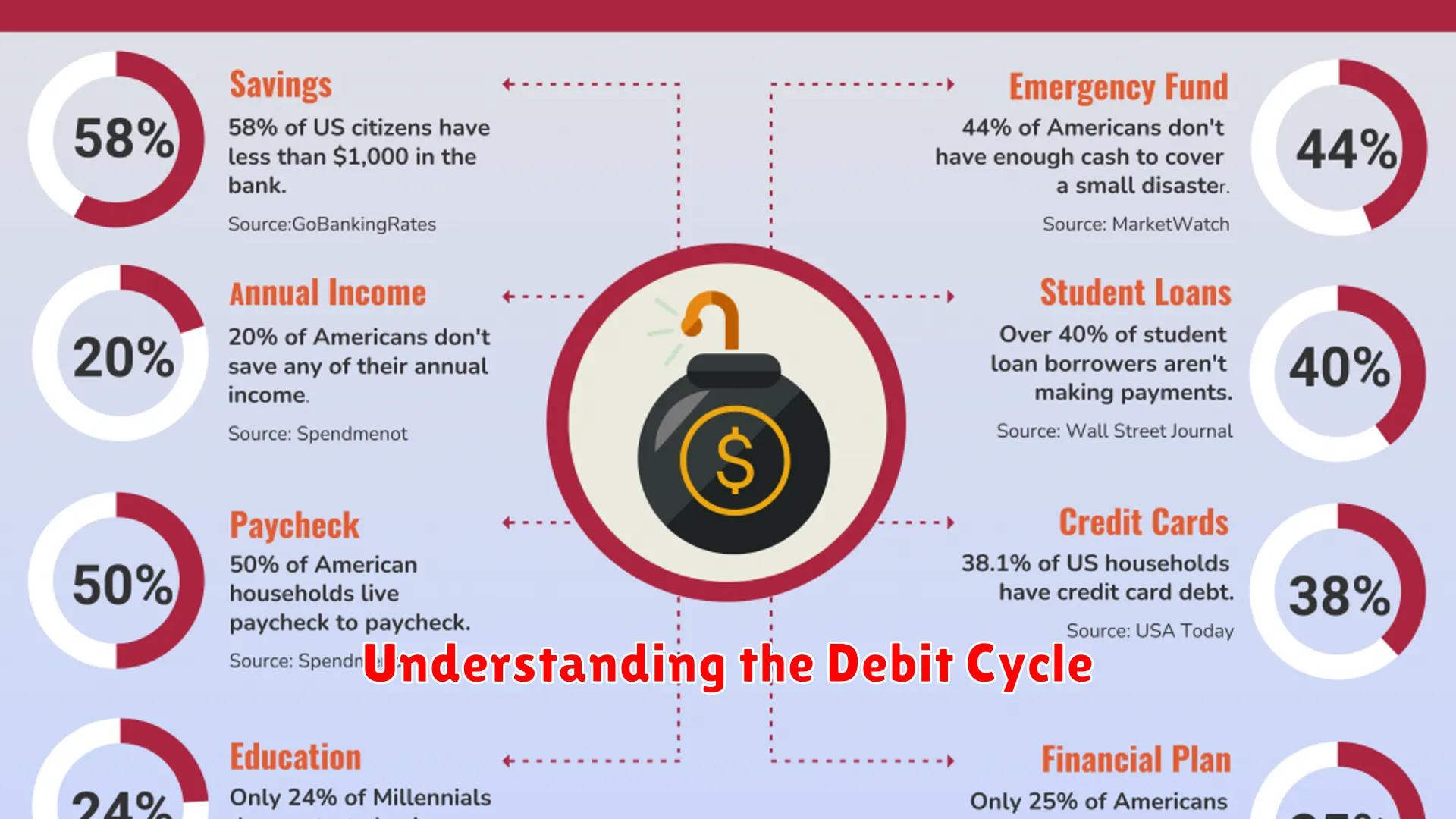

Understanding the Debit Cycle

In the realm of personal finance, understanding the debit cycle is crucial for individuals looking to take control of their financial well-being. The debit cycle refers to the process by which funds are withdrawn directly from a checking account to cover purchases, bills, or expenses. Breaking the debit cycle involves implementing proven strategies to effectively manage and improve your financial situation.

One key aspect of understanding the debit cycle is tracking your expenses diligently. By keeping a close eye on where your money is going, you can identify patterns and areas where you may be overspending. This awareness allows you to make informed decisions and adjust your spending habits to break the cycle of unnecessary purchases.

Moreover, creating a budget is a fundamental step in managing the debit cycle. Setting limits on various categories of spending, such as groceries, entertainment, and utilities, empowers you to allocate funds sensibly and avoid dipping into overdraft territory. Budgeting helps prevent the accumulation of debt and ensures that you live within your means.

Another strategy to break the debit cycle is to automate your savings. By automatically transferring a portion of your income to a savings account before you have a chance to spend it, you prioritize building a financial safety net. This habit not only shields you from unexpected expenses but also cultivates a mindset of long-term financial planning.

Ultimately, understanding the debit cycle is about taking proactive steps to manage your finances responsibly. By gaining insights into your spending patterns, setting clear financial goals, and adhering to a budget, you can pave the way for a brighter financial future free from the constraints of the debit cycle.

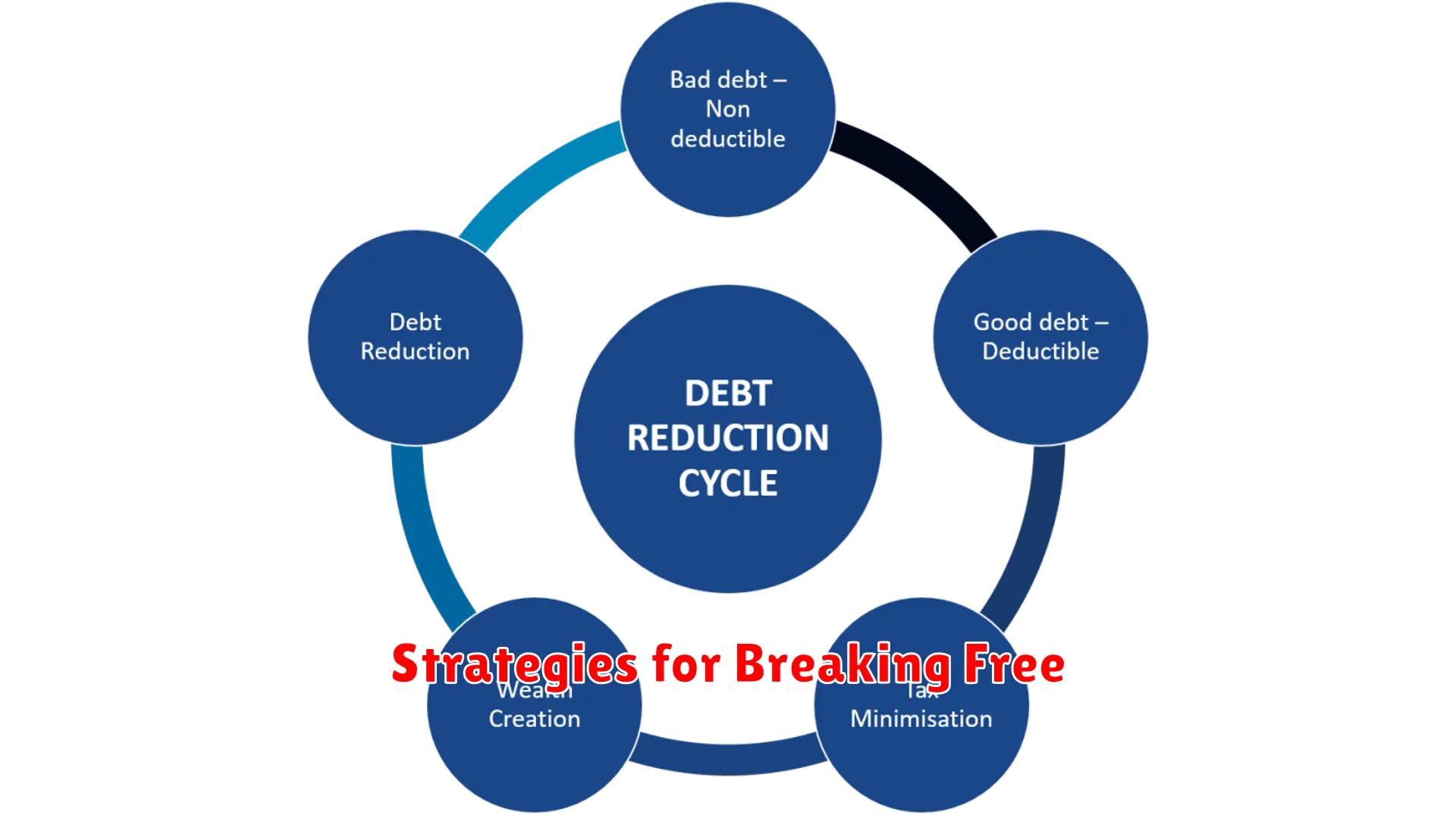

Strategies for Breaking Free

Breaking the debit cycle and achieving a brighter financial future involves implementing effective strategies to gain control over your finances and build a solid foundation for financial stability. Here are some proven strategies to help you break free from the cycle of debt:

1. Create a Budget and Stick to It

The first step in breaking free from the debit cycle is to create a comprehensive budget that outlines your income, expenses, and financial goals. Identify areas where you can cut back on spending, prioritize essential expenses, and allocate a portion of your income towards debt repayment.

2. Build an Emergency Fund

Having an emergency fund can provide a safety net and help prevent you from relying on credit cards or loans in times of unexpected expenses. Aim to save a minimum of three to six months’ worth of living expenses in an easily accessible account.

3. Consolidate and Refinance Debts

If you have multiple debts with high-interest rates, consider consolidating them into a single, more manageable loan with a lower interest rate. Refinancing can help lower your monthly payments and simplify your debt repayment process.

4. Increase Your Income

Explore ways to boost your income, such as taking on a part-time job, freelancing, or selling unused items. Use the additional income to accelerate debt repayment and improve your financial situation.

5. Seek Professional Help

If you’re struggling to break free from the debit cycle on your own, consider seeking the help of a financial advisor or credit counselor. They can provide personalized guidance, negotiate with creditors on your behalf, and create a debt management plan tailored to your needs.

By implementing these strategies and staying committed to your financial goals, you can break free from the debit cycle, regain control over your finances, and pave the way for a brighter financial future.

The Importance of a Support System

In the journey towards breaking the debit cycle and securing a brighter financial future, having a strong support system is essential. Your support system consists of individuals who believe in your goals, provide encouragement, and offer practical assistance when needed.

Emotional Support

One critical aspect of a support system is the emotional support it provides. During challenging times, having people to listen, empathize, and uplift you can make a significant difference in your mindset and motivation. Surrounding yourself with positivity and understanding can help you stay focused on your financial goals.

Accountability Partner

Another key role of a support system is having an accountability partner. This individual can help keep you accountable for your financial decisions and commitments. By regularly discussing your progress and setbacks with someone you trust, you can stay on track and avoid falling back into old habits.

Financial Guidance

Seeking the guidance of individuals with financial expertise can also be invaluable. Whether it’s a financial advisor, a mentor, or a knowledgeable friend, having access to sound financial advice can help you make informed decisions and develop a sustainable financial plan.

Shared Resources

Your support system can also provide access to shared resources that can help you save money, earn extra income, or learn new financial skills. Collaborating with your support network to explore opportunities such as budgeting tools, investment strategies, or side hustles can enhance your financial journey.

Tools and Resources for Debit Management

Effective management of your debit is crucial for maintaining a healthy financial future. Here are some valuable tools and resources to help you break the debit cycle and take control of your finances:

1. Budgeting Apps

Utilize budgeting apps such as Mint, YNAB (You Need a Budget), or Personal Capital to track your expenses, set financial goals, and create a realistic budget that works for you. These apps can provide insights into your spending habits and help you identify areas where you can cut back.

2. Debt Repayment Calculators

Use debt repayment calculators available online to devise a repayment plan for your debts. These calculators can show you how long it will take to pay off your debt based on different payment amounts and interest rates, empowering you to make informed decisions.

3. Credit Counseling Services

Consider seeking help from credit counseling services like the National Foundation for Credit Counseling (NFCC) or local non-profit organizations. These services offer personalized advice, debt management plans, and financial education to assist you in managing your debt effectively.

4. Financial Literacy Resources

Enhance your financial knowledge by accessing financial literacy resources such as workshops, seminars, and online courses. Organizations like the Consumer Financial Protection Bureau (CFPB) and educational websites like Investopedia provide valuable information on managing debt and improving financial wellness.

5. Debt Consolidation Options

Explore debt consolidation options like balance transfer credit cards, debt consolidation loans, or home equity loans. Consolidating your debts can simplify your repayment process, potentially lower your interest rates, and help you become debt-free sooner.

Building a Brighter Financial Future

Breaking the debit cycle and setting yourself up for a brighter financial future requires a strategic approach and disciplined financial habits. By implementing proven strategies, you can take control of your finances and pave the way for a more secure financial outlook.

Evaluate Your Spending Habits

Start by conducting a thorough evaluation of your spending habits. Look closely at where your money is going each month and identify areas where you can cut back. This awareness is key to making meaningful changes and breaking free from the cycle of overspending.

Create a Realistic Budget

Develop a realistic budget that outlines your income and expenses. Be sure to allocate funds for necessities such as rent, utilities, and groceries, as well as for savings and debt repayment. A well-planned budget serves as a roadmap for your financial future.

Focus on Debt Repayment

Prioritize debt repayment to reduce financial stress and interest charges. Consider using the snowball or avalanche method to tackle your debts systematically. By making extra payments towards your debts, you can expedite the repayment process and build momentum towards a debt-free future.

Establish an Emergency Fund

Set up an emergency fund to cover unexpected expenses and avoid relying on credit cards or loans. Aim to save at least three to six months’ worth of living expenses in a separate account. This fund acts as a safety net during challenging times and prevents a setback in your financial progress.

Invest in Your Future

Look towards the future by investing in long-term financial goals such as retirement or education. Consider opening a tax-advantaged retirement account or setting up a college savings plan for your children. By starting early and consistently contributing, you can secure a more stable financial future for yourself and your loved ones.

Conclusion

By implementing these proven strategies, breaking the debit cycle and securing a brighter financial future is achievable for anyone willing to make proactive changes in their financial habits.

{kind=link}